I tend to repeat that, in the long term, stocks are less likely than bonds to lose purchasing power, that stocks are scary but it is bonds that are risky and overall that in the long term you must try to make money, not to avoid losing some.

If it were this easy, everyone would do it (it is probably not true, but never mind). For a long-term investment, the rule of thumb is to choose the highest stock allocation you can maintain over the life of the investment. As much equity as possible because it increases the average gains, while reducing the risk of losses over the investment term. But not to the point of scaring you, if that means selling at the bottom.

And it is this latter criterion that creates most of the trouble. On the one hand, this is because it varies from person to person, so I cannot answer the question properly in your case without knowing you. On the other hand, the questionnaires used to evaluate your "risk profile" talk about risk in general and ask vague questions with no clear relevance to the subject.

In theory, however, things are clear and simple: in the long term equities have only advantages over bonds. Except that before you reach the long term, they can lose a lot of money very brutally. So you should not have too much equity, that is to say a portfolio that might scare you.

Instead of questionnaires, I prefer a more direct approach: putting on the shoes of an investor during a crash. In 1973–1974, global stock markets fell heavily — how would you react to this turbulence? (One can use a scale from "Really, something happened?" to "Mommy, help!".)

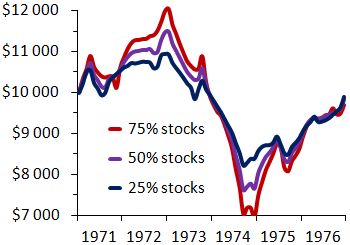

An investment of $10 000 in early 1971 with three quarters in equity and one quarter in bonds (red curve in the figure below) grew to $12 000 in two years, and then fell to $7 000 two years later. It means a 30% loss of purchasing power on the initial capital, and even a little more than 40% from the high of January 1973 (stocks themselves lost 50%).

Figure: Investments of $10 000 in 1971 in stock–bond portfolios.

How would you react if your $10 000 investment were worth only $7 000 four years later? How would you react if your capital were down to $7 000 two years after reaching $12 000? (Of course, the figure also shows that the price then rebounded, and nearly returned to the initial capital in December 1976, but when the stock market is falling, one sees only this fall, and it is quite difficult to think about the rise that is to follow.)

An investment 25% in stocks and 75% in bonds (dark blue line) would, however, have lost only a quarter of its value between top and bottom. The loss was a third for a half-stock half-bond investment (purple). In the long term these investments return less on average than an investment with more equity, but the falls are also less steep. If the drop of the portfolio with a majority of equity terrifies you, you would be better off with more bonds, to sleep better at night.

Will such a portfolio return less than one with more equity? Yes in theory. But if it prevents you from panicking and selling after the fall then probably not.

Note: The figure, based on the S&P 500 and US bonds for the period 1871–2014, is only intended as an indication of general trends in stocks and bonds.