When talking about risk, one generally refers to stocks, not bonds. After all, what is the probability for bonds to lose 20% or 30% of their values in less than a year? No really, dear, risk is in stocks.

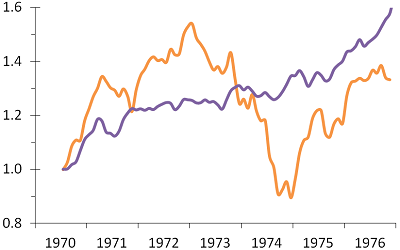

Figure 1 shows that shares and bonds do not behave the same way in the short-to-medium term. Stocks (orange line) tend to gain a lot of ground, fall violently and then recover and bounce back as quickly as they fell. It gives an N-shaped curve. In contrast, bonds (in purple) increase more slowly and smoothly.

Figure 1: The evolution of the value before inflation of stocks (orange) and bonds (purple) over the period 1970–1976.

These sudden changes in stock prices, called volatility, are what is generally referred to as the risk. It makes for great news flashes and everyone is aware that the stock market can fall sharply. If this were the whole story then clearly stocks would be riskier than bonds. Okay shares are very scary, but are they really what is most dangerous?

For starters, one can readily see that the drop is abrupt but short-lived. The fall of shares from market top to bottom is deep, but it follows a gain of more than 50% in two and a half years, and it is followed by a rebound. If we look at what happens a bit before and a bit after the crash (say over 1972–1975), we see that stocks did not really lose money.

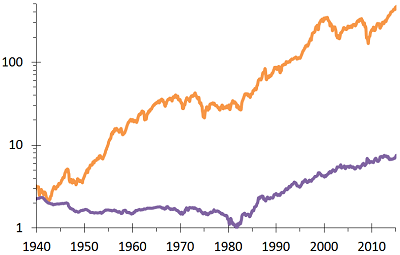

Figure 2 focuses on the evolution of the purchasing power of shares and bonds in the longer run, that is to say, unlike Fig. 1, it accounts for inflation. At this scale, what one sees is a steady rise of stocks (hundred-fold increase in purchasing power, not bad) with some blips on a smaller scale. And for bonds, one sees four decades without gains or with losses (halving the purchasing power) and a recovery over the following thirty years. This loss is generally due to inflation, and when inflation sets in it does not go away just like that.

Figure 2: The evolution of the purchasing power of stocks (orange) and bonds (purple) over the period 1940–2014.

There is on the one hand the risk of a violent but temporary drop in the short-to-medium term for stocks, and on the other the risk of bonds slowly bleeding to death. The former is scarier, but does it hurt more? For my part, what scares me is a long-term investment that earns me nothing for decades, not an investment that may lose value temporarily before recovering. The shares are scarier (short term) but bonds can do more harm (long term).

NB: The figures, based on the S&P 500 and US treasuries, are only intended to indicate general trends of stocks compared to bonds.